Once again the Obama Department of Justice has reached a settlement with a To Big To Fail Bank for pennies on the dollar and let the perpetrators walk away without criminal sanctions or penalties. Goldman Sachs will pay $5.06bn for its role in the 2008 financial crisis, the US Department of Justice said on Monday. …

Tag: Goldman Sachs

Jul 24 2013

Hoarding Commodities: Big banks making a buck off of…a can of soda?

In the New York Times late last week there was a report how Goldman Sachs is manipulating aluminum commodities that is costing American consumer billions of dollars. This is how it works:

The story of how this works begins in 27 industrial warehouses in the Detroit area where a Goldman subsidiary stores customers’ aluminum. Each day, a fleet of trucks shuffles 1,500-pound bars of the metal among the warehouses. Two or three times a day, sometimes more, the drivers make the same circuits. They load in one warehouse. They unload in another. And then they do it again.

This industrial dance has been choreographed by Goldman to exploit pricing regulations set up by an overseas commodities exchange, an investigation by The New York Times has found. The back-and-forth lengthens the storage time. And that adds many millions a year to the coffers of Goldman, which owns the warehouses and charges rent to store the metal. It also increases prices paid by manufacturers and consumers across the country. [..]

Only a tenth of a cent or so of an aluminum can’s purchase price can be traced back to the strategy. But multiply that amount by the 90 billion aluminum cans consumed in the United States each year – and add the tons of aluminum used in things like cars, electronics and house siding – and the efforts by Goldman and other financial players has cost American consumers more than $5 billion over the last three years, say former industry executives, analysts and consultants.

All In host Chris Hayes spoke with Sen. Sherrod Brown (D-OH) about the newly revealed practice by Goldman Sachs to skirt price regulations on a product we use every day-aluminum-costing American consumers billions of dollars and it ain’t just aluminum.

U.S. Weighs Inquiry Into Big Banks’ Storage of Commodities

by Gretchen Morgenson and David Kocieniewski, New York Times

The overarching question is whether banks should control the storage and shipment of commodities, and whether such activities could pose a risk to the nation’s financial system.

But other crucial issues are expected to arise as well. Among them is how Wall Street’s push into these markets has affected the prices paid by manufacturers and ultimately consumers. Another is whether Goldman and Morgan Stanley have operated their storage facilities at arms’ length from their banking business, as required by regulators.

Goldman has exploited industry pricing regulations set by the London Metal Exchange by shuffling tons of aluminum each day among the 27 warehouses it controls in the Detroit area, The Times reported on Sunday. The maneuver lengthens the storage time and generates millions a year in profit for Goldman, which charges rent to store the metal for customers, the investigation found. The C.F.T.C. issued the notices late last week, and it was unclear on Monday whether the agency or other authorities would open a full-fledged investigation into banks’ activities.

Senate Scrutiny of Potential Risk in Markets for Commodities

by Edward Wyat, New York Times

The hearing, convened by the Senate Financial Institutions and Consumer Protection subcommittee, came as Goldman Sachs, JPMorgan Chase and others face growing scrutiny over their role in the commodities markets and the extent to which their activities can inflate prices paid by manufacturers and consumers. The Federal Reserve is reviewing the potential risks posed by the operations, which have generated many billions of dollars in profits for the banks. [..]

Several witnesses at Tuesday’s hearings warned that letting the country’s largest financial institutions own commodities units that store and ship vast quantities of metals, oil and the other basic building blocks of the economy could pose grave risks to the financial system. The ability of those bank subsidiaries to gather nonpublic information on commodities stores and shipping also could give the banks an unfair advantage in the markets and cost consumers billions of dollars, the witnesses said.

Goldman Sachs isn’t alone in this game.

Not Just Goldman Sachs: Koch Industries Hoards Commodities as a Trading Strategy

by Lee Fang, The Nation

Worth noting: Koch Industries, a company often inaccurately described as simply an oil or manufacturing concern, is highly active in the commodity speculation business akin to the big hedge funds and banks like Goldman Sachs.

As Fortune magazine reported, when oil prices dropped from a record high in July of 2008 to record lows in December of that year, Koch bought up the cheap oil to take it off of the market. Koch leased a number of giant oil tankers, including the 2-million-barrel-capacity Dubai Titan, to store the oil offshore. The decrease in supply increased the price for consumers that year, while Koch took advantage of selling the oil off later at higher prices.

Koch Industries’ executive David Chang later boasted, “The drop in crude oil prices from more than US$145 per barrel in July 2008 to less than US$35 per barrel in December 2008 has presented opportunities for companies such as ours. In the physical business, purchases of crude oil from producers and storing offshore in tankers allow us to benefit from the contango market where crude prices are higher for future delivery than for prompt delivery.”

The company took advantage when the prices were low, but they also gained when the prices were high. A leaked document I obtained shows Koch among the largest traders (including Goldman Sachs and Morgan Stanley) speculating on the price of oil in the summer of 2008.

Elizabeth Warren Wants To Take This Goldman Sachs Aluminum Story And Run Right Over Wall Street With It

by Linette Lopez, Business Insider

Back in 2003 the Federal Reserve decided to temporarily allow banks to purchase commodities directly. That means oil, power, copper, aluminium etc. This September, that temporary regulatory relaxation is set to expire, and if it does, a big chunk of Wall Street’s business will expire with it.

And now that the ruling is up for discussion, Congress gets to weigh in. Wall Street be warned, if this hearing was any indication, the Senate is coming down on the side of culling the commodities business.

Warren decried the idea that banks would use “other people’s money” in pension and retirement savings “to pave the way for big banks to be able to control an electric plant or an oil refinery.” [..]

The witnesses didn’t just talk about prices either, they talked monopolies. Since her rise to prominence as a regulator and then a Senator, Warren has been saying that banks are getting too big, too interconnected, and too complicated. (Joshua) Rosner’s testimony corroborated that idea, and added to it the specter of commodities

controlling, allencompassing banking behemoths backstopped by the government (too big too fail).

It is more than past time to break up these banks and for the Federal Reserve to be more transparent in how it regulates the banks.

May 20 2013

Barack Obama, Occupy Wall Street and Martin Luther King’s Mission and Legacy

Barack Obama is the largest governmental obstacle to the continuation and completion of Martin Luther King’s mission.

Bill Moyers had an excellent conversation with James Cone and Taylor Branch about what could be called, “MLK’s unfinished business;” Moyers called it, “James Cone and Taylor Branch on MLK’s Fight for Economic Equality.” I recommend checking out the whole conversation, which starts out this way:

You may think you know about Martin Luther King, Jr., but there is much about the man and his message we have conveniently forgotten. He was a prophet, like Amos, Isaiah and Jeremiah of old, calling kings and plutocrats to account, speaking truth to power.

Yet, he was only 39 when he was murdered in Memphis, Tennessee on April 4th, 1968. The March on Washington in ’63 and the March from Selma to Montgomery in ’65 were behind him. So were the passage of the Civil Rights Act and the Voting Rights Act. In the last year of his life, as he moved toward Memphis and fate, he announced what he called the Poor People’s Campaign, a “multi-racial army” that would come to Washington, build an encampment and demand from Congress an “Economic Bill of Rights” for all Americans – black, white, or brown. He had long known that the fight for racial equality could not be separated from the need or economic equity – fairness for all, including working people and the poor. That’s why he was in Memphis, marching with sanitation workers on strike for a living wage when he was killed.

Popular notions of Martin Luther King’s work celebrate his mission as one that was fundamentally about racial justice. Moyers and his guests point out that this conventional wisdom seriously understates the scope and scale of King’s vision and mission. King’s mission was not only to advance the interests of African-Americans but to demand and implement a culture of social and economic justice.

Feb 21 2013

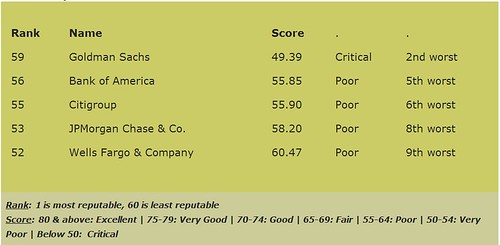

Five biggest TBTF banks are among least reputable companies in America

Harris Interactive’s annual “Reputation Quotient” survey for 2013 finds that the five biggest “too big to fail” (TBTF) U.S. banks have some of the lowest reputations in the country according to their survey of the general public. All five of them are ranked in the lowest eight slots among the sixty most visible companies measured.

The maximum “reputation quotient” is 100. Any quotient lower than 64 is considered to be “poor” and anything below 50 is considered “critical”. All of the big five TBTF banks scored lower than 64 and Goldman Sachs is below 50, so its reputation is in “critical” condition.

Bank of America and JP Morgan have seen some improvement in their score this year, but their reputation still falls into the “poor” range.

Harris Interactive also ranks industry reputations. The banking and financial services industries rank above only two other industries: government and tobacco. Banking and financial services have improved over last year, however, by seven and eight percentage points, respectively. Technology, travel and retail are the top three.

This poll has been published for fourteen consecutive years. This year, more than fourteen thousand interviews were conducted for data collection.

Bank Size (1 is the largest)

Harris Reputation Index

Sources:

FFIEC – Top 50 holding companies (HCs) as of 12/31/201

relbanks.com – The Largest US Banks

The Harris Poll 2013 RQ® Summary Report – A Survey of the U.S. General Public Using the Reputation Quotient® (This file is a PDF)

Feb 13 2013

The Real SOTU: The White House Subverting the Rule of Law

Subverting the rule of law? How dare I? Well the 4th amendment, due process, kill lists, and the NDAA also speak to my title. Yes, they speak to it despite those that decided politicians were more important than the principles they pretended to have in 2004 now outed as hypocrites mostly. However, that being said, I’m talking about subverting the rule of law in a different way but equally as damaging on the economic front.

After all, it was at the SOTU merely just a year ago that President Obama assured us that something was going to be done about the Wall St. perpetrators of our mortgage and foreclosure crisis. This was a crisis in which they defrauded consumers with sub-prime NINJA loans pumping up the housing bubble and then dumping the private debt overhang onto the economy destroying over 10 trillion in housing wealth. This left consumers with massive loads of private debt and everyone else jobless like this recovery.

This White House’s DOJ has made a complete mockery of the concept of Justice in and of itself. That illusion of Justice is perpetuated to this day and normal people are devastated because of it. Let President Obama know you are not amused. I have.

Nov 28 2012

WH Advisor David Plouffe and Goldman Sachs CEO Agree That Medicare and Medicaid Must be Cut

Yes, it’s true. If the White House would like to disavow David Plouffe’s words now is the time. Time is running short but it’s pretty obvious that he speaks for the White House given that David Plouffe is the President’s closest confidante. If you have the stomach to sit through this forum it’s right there for you to see, but I’ll post the relevant portion that matches up with Lloyd Blankfein’s mentality that the 99% need to sacrifice Medicare and retire later for the fantasy deficit crisis he, the White House, and Congress are peddling to the American people.

The President’s closest adviser is telling his base that additional cuts to pay down the deficit(not the 716 billion to Advantage, fraud, or providers from the 2010 CBO baseline on the effects of the ACA) in Medicare and Medicaid are coming and to be ready for them.

“The only way that gets done is for Republicans again to step back and get mercilessly criticized by Grover Norquist and the Right, and it means that Democrats are going to have to do some tough things on spending and entitlements that means that they’ll criticized on by their left,” Plouffe said at his alma mater in conversation with former McCain campaign manager Steve Schmidt.

[………]

Plouffe added that while the White House wants to engage in comprehensive tax reform, they know they must also “carefully” address the “chief drivers of our deficit”: Medicare and Medicaid.

Lloyd “Sell them shitty deals with the blessing of the US DOJ” Blankfein whole heartedly agrees with Plouffe. He’s also visiting the White House today. I have a feeling whatever good feelings labor and progressive groups had yesterday were perhaps misguided given the statement we just heard from David Pouffe. That and of course basically the priority of making capital whole on the backs of labor as 93% of the “recovery” goes into Lloyd Blankfein’s pocket since 2010.

Goldman Sachs CEO: Entitlements must be contained

BLANKFEIN: You’re going to have to undoubtedly do something to lower people’s expectations — the entitlements and what people think that they’re going to get, because it’s not going to — they’re not going to get it.

PELLEY: Social Security, Medicare, Medicaid?BLANKFEIN: You can look at history of these things, and Social Security wasn’t devised to be a system that supported you for a 30-year retirement after a 25-year career. … So there will be things that, you know, the retirement age has to be changed, maybe some of the benefits have to be affected, maybe some of the inflation adjustments have to be revised. But in general, entitlements have to be slowed down and contained.

Mar 15 2012

Goldman Sachs “Old Days” Not So Rosy Either

A Goldman Sachs executive resigned in a lengthly and scathing op-ed in the New York Times. Greg Smith worked at Goldman Sachs for 12 years, rising to executive director and head of the firm’s United States equity derivatives business in Europe, the Middle East and Africa. His latter shreds Goldman Sachs policies and employees:

To put the problem in the simplest terms, the interests of the client continue to be sidelined in the way the firm operates and thinks about making money. Goldman Sachs is one of the world’s largest and most important investment banks and it is too integral to global finance to continue to act this way. The firm has veered so far from the place I joined right out of college that I can no longer in good conscience say that I identify with what it stands for […]

How did we get here? The firm changed the way it thought about leadership. Leadership used to be about ideas, setting an example and doing the right thing. Today, if you make enough money for the firm (and are not currently an ax murderer) you will be promoted into a position of influence.

What are three quick ways to become a leader? a) Execute on the firm’s “axes,” which is Goldman-speak for persuading your clients to invest in the stocks or other products that we are trying to get rid of because they are not seen as having a lot of potential profit. b) “Hunt Elephants.” In English: get your clients – some of whom are sophisticated, and some of whom aren’t – to trade whatever will bring the biggest profit to Goldman. Call me old-fashioned, but I don’t like selling my clients a product that is wrong for them. c) Find yourself sitting in a seat where your job is to trade any illiquid, opaque product with a three-letter acronym.

Smith lays the blame for this climate of greed at the feet Goldman’s CRO, Lloyd Blankfein and the company’s president, Gary Cohn.:

When the history books are written about Goldman Sachs, they may reflect that the current chief executive officer, Lloyd C. Blankfein, and the president, Gary D. Cohn, lost hold of the firm’s culture on their watch. I truly believe that this decline in the firm’s moral fiber represents the single most serious threat to its long-run survival.

Matt Taibbi at Rolling Stone asks, like Forbes, should clients fire Goldman:

Banking, and finance, is a business that has to be first and foremost about trust. The reason you’re paying your broker/money manager such exorbitant sums is because that’s the value of integrity and honesty: You’re paying for the comfort of knowing he has your best interests at heart.

But what we’ve found out in the last years is that these Too-Big-To-Fail megabanks like Goldman no longer see the margin in being truly trustworthy. The game now is about getting paid as much as possible and as quickly as possible, and if your client doesn’t like the way you managed his money, well, fuck him – let him try to find someone else on the market to deal him straight.

These guys have lost the fear of going out of business, because they can’t go out of business. After all, our government won’t let them. Beyond the bailouts, they’re all subsisting daily on massive loads of free cash from the Fed. No one can touch them, and sadly, most of the biggest institutional clients see getting clipped for a few points by Goldman or Chase as the cost of doing business.

Speaking at the Atlantic Economy Summet in Washington, DC, former Federal Reserve Chairman, Paul Volker, said that Smith’s letter proves the need for the his rule

“[Trading] is a business that leads to a lot of conflicts of interest. You’re promised compensation when you’re doing well, and that’s very attractive to young people. All these firms can attract the best of American graduates, whether they’re philosophy majors or financial engineers, it didn’t make any difference,” Volcker said.

“A lot of that talent was siphoned off onto Wall Street. But now we have the question of how much of that activity is really constructive, in terms of improving productivity in the GDP,” Volcker said. “These were brilliant years for Wall Street by one perspective, but were they brilliant years for the economy? There’s no evidence of that. The rate of economic growth did not pick up, the rate of productivity did not pick up, the average household had no increase in their income over this period, or virtually no increase.”

Volcker noted that commercial banks hold the money of average Americans, and are insured by the federal government. “Should the government be subsidizing or protecting institutions that…are essentially engaged in speculative activities, often at the expense of customer relations?”

Yves Smith at naked capitalism, who also has been at the Atlantic conference weighed in that those good old days of the ’90’s weren’t as “rosy” as Smith remembers:

Earth to Greg: the old days were not quite as rosy as you suggest, but it is true that Goldman once cared about the value of its franchise, and that constrained its behavior. So it was “long term greedy,” eager to grab any profit opportunity but concerned about its reputation. I knew someone who was senior in what Goldman called human capital management, and even though, in classic old Goldman style, he was loath to say anything bad about anyone, he was clearly disgusted of Lloyd Blankfein and the crew that took over leadership after Hank Paulson, John Thain and John Thornton departed. Before the firm before had gone to some lengths to preserve its culture and was thoughtful about how to operate the firm. One head of a well respected investment bank told me in the mid 1990s: “It isn’t that Goldman has better people. All the top firms have good people. It’s that they make the effort to manage themselves better than anyone else.” That apparently went out the window when Blankfein came in. My contact said all his cohort cared about was how much money they could make in the current year.

Wall St. responded defensively calling Smith a “small timer” having a “midlife crisis“. That “crisis” so far has lost Goldman $2.5 billion in its market value:

The shares dropped 3.4 percent in New York trading yesterday, the third-biggest decline in the 81-company Standard & Poor’s 500 Financials Index, after London-based Greg Smith made the accusations in a New York Times op-ed piece.

Stephen Colbert “disapproves” of Greg Smith, after all Lloyd Blankfeid said Goldman was just doing “God’s work.”

Jun 29 2011

Take The Money And Run

After receiving a $10 billion of tax payer money in the financial crisis bailout and making a record $2.7 billion profit in the first quarter of 2011, Goldman Sachs will lay off 1,000 American workers and out source their jobs to Singapore.

After receiving a $10 billion of tax payer money in the financial crisis bailout and making a record $2.7 billion profit in the first quarter of 2011, Goldman Sachs will lay off 1,000 American workers and out source their jobs to Singapore.

The jobs in Singapore are likely to be “high-paying, skilled positions in sales and investment banking,” the same types that are likely to be cut in the firm’s domestic operations, according to one person with knowledge of the matter. This person added that the firm has recently briefed people in Washington about the new overseas jobs because it “is afraid of the fallout” as it plans to slash $1 billion in costs over the next year — a move that will mean a significant, though still undetermined number of layoffs across its operations, though people close to the firm expect the biggest hit to come from the US. Goldman also plans a much smaller expansion in its Brazil unit and in India.

Last year, the Republicans in the Senate, aided by Sen Joe Lieberman and four Democrats, blocked a bill that would have ended tax breaks for companies that shift American jobs overseas. Over the last decade these mega corporations have laid off nearly 3 million American while hiring 2.4 million overseas. These jobs are not low tech jobs as these companies claim but but jobs held by highly educated workers who never expected to find themselves among the unemployed.

Jun 02 2011

Goldman Sachs Gets Subpoenas From NYC DA

Leave it to the District Attorney of Manhattan to do what the Obama DOJ failed to do, investigate properly the fraud that led to the economic crisis.

Goldman Receives Subpoena Over Financial Crisis

By Andrew Ross Sorkin and Susanne Craig

Goldman Sachs has received a subpoena from the office of the Manhattan district attorney, which is investigating the investment bank’s role in the financial crisis, according to people with knowledge of the matter.

The inquiry stems from a 650-page Senate report from the Permanent Subcommittee on Investigations that indicated Goldman had misled clients and Congress about its practices related to mortgage-linked securities.

Senator Carl Levin, Democrat of Michigan, who headed up the Congressional inquiry, had sent his findings to the Justice Department to figure out whether executives broke the law. The agency said it was reviewing the report.

The subpoena come two weeks after lawyers for Goldman Sachs met with the attorney general of New York’s office for an “exploratory” meeting about the Senate report, the people said.

From Talking Points Memo:

Manhattan DA Subpoenas Goldman Sachs Over Financial Crisis

The subpoena is apparently based on information contained in a Senate Permanent Subcommittee on Investigations report on Wall Street’s role in the housing market collapse. The report was critical of Goldman Sachs, and accused the bank of misleading buyers of mortgage-linked investments.

May 15 2011

Poor Goldman Sachs, Those Laws Are Just Too Confusing

Poor Goldman Sachs. According to Megan McArdle, one of the Atlantic Monthly’s Wall St apologists, argued on CNN’s Your Money in a debate with Rolling Stone’s Matt Taibbi that the laws were too confusing and it would be too hard to figure out ig they did anything wrong. While conversely, she insinuates that those who the toxic assets were sold to should have known what they were buying. Let’s blame the victims. Megan even admits that she hasn’t read all the documents while Taibbi has. How does Megan have any credibility on this is beyond comprehension. Here are some of the “high” points from the transcript of the video:

MCARDLE: What we have to do is disclose. It’s perfectly legal for a dealership to sell me a car I’m not going to like or that’s too expensive for me. It’s not legal for them to sell me a car that’s not what they represented it as.

And we set certain legal minimum standards and that’s what happened here. At least, John Losera and all the devils who are here argues that he actually has gone through these documents and says that a lot of these things were disclosed. That in fact Goldman laid out in very lengthy detail all of the ways in which this could go wrong. I haven’t read the disclosure documents personally.

TAIBBI: I have.

MCARDLE: There are two competing versions of the story.

VELSHI: Matt, you’ve read them?

TAIBBI: Well, I’ve read all the documents in this report and I’ve also talked to some of the principals in this entire story. I definitely know some of the client that is Goldman was talking about were completely blindsided by the fact that, for instance.

They were buying assets out of Goldman’s own book when they were told that Goldman was buying these assets off the street. They definitely did not make key disclosures that they were legally obligated to make.

The People vs. Goldman Sachs

By Matt Taibbi

A Senate committee has laid out the evidence. Now the Justice Department should bring criminal charges

They weren’t murderers or anything; they had merely stolen more money than most people can rationally conceive of, from their own customers, in a few blinks of an eye. But then they went one step further. They came to Washington, took an oath before Congress, and lied about it.

Thanks to an extraordinary investigative effort by a Senate subcommittee that unilaterally decided to take up the burden the criminal justice system has repeatedly refused to shoulder, we now know exactly what Goldman Sachs executives like Lloyd Blankfein and Daniel Sparks lied about. We know exactly how they and other top Goldman executives, including David Viniar and Thomas Montag, defrauded their clients. America has been waiting for a case to bring against Wall Street. Here it is, and the evidence has been gift-wrapped and left at the doorstep of federal prosecutors, evidence that doesn’t leave much doubt: Goldman Sachs should stand trial.

What’s so hard to fathom, Megan? They committed fraud and then lied about the fraud. Lloyd Blenkenfein isn’t too big for a cell next to Bernie Madoff. The Justice Department and Eric Holder needs to get its act together.

- 1

- 2

Recent Comments