David Dayen may have hit the nail on the head when he wrote about the latest Super Committee’s wrangling over using Social Security to pay for the 1%’s tax cuts:

I don’t have to tell you about how Social Security never contributed one penny to the deficit. It holds a surplus of $2.6 trillion, and the elites just don’t want to pay off the trust fund because that might mean higher taxes on rich people. A bargain was made 30 years ago to build up the trust fund and pay for the baby boomers’ retirement, and now they want to renege on that deal and take the money out of the hides of old pensioners.

I assume that the effort here is to move to chained CPI, which will lead to a reduction in benefits. It’s also a regressive tax increase. If the leaders in Washington think that a public already out in the streets over inequality, Wall Street greed and corporate control of government will meekly accept that, they’re just wrong.

Of course, members of Congress won’t really have to worry about their benefits getting cut. That’s because they’re mostly fabulously wealthy and won’t be burdened as much as the other 99% by a more meager Social Security check every month.

The front page article in the Washington Post that got everyone’s dander up this week is so blatantly wrong that is a bold faced lie that has been debunked numerous times. Economist Dean Baker was much kinder saying that the “Washington Post Discards All Journalistic Standards In Attack on Social Security”:

The basic premise of the story, as expressed in the headline (“the debt fallout: how Social Security went ‘cash negative’ earlier than expected”) and the first paragraph (“Last year, as a debate over the runaway national debt gathered steam in Washington, Social Security passed a treacherous milestone. It went ‘cash negative.'”) is that Social Security faces some sort of crisis because it is paying out more in benefits than it collects in taxes. [The “runaway national debt” is also a Washington Post invention. The deficits have soared in recent years because of the economic downturn following the collapse of the housing bubble. No responsible newspaper would discuss this as problem of the budget as opposed to a problem with a horribly underemployed economy.]

This “treacherous milestone” is entirely the Post’s invention, it has absolutely nothing to do with the law that governs Social Security benefit payments. Under the law, as long as there is money in the trust fund, then Social Security is able to pay full benefits. There is literally no other possible interpretation of the law.

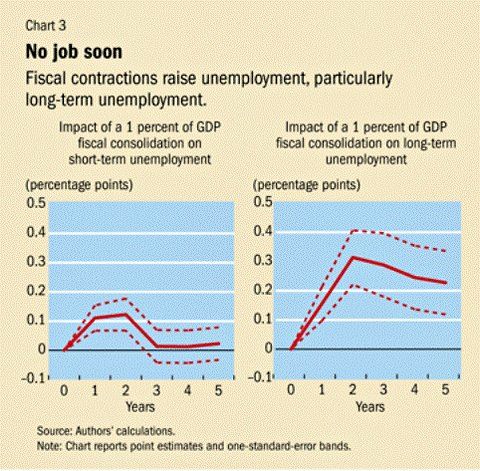

Dean rips apart the proposal by former Senator Alan Simpson and Morgan Stanley director Erskine Bowles that emerged form President Obama’s failed Cat Food Commission I:

Actually the plan put forward by Bowles and Simpson would have implied large cuts for most low-income workers who would not have met the work requirements needed for the higher benefit. The cut would have taken the form of a 0.3 percentage point reduction in the annual cost of living adjustment. This cut would be cumulative, after 15 years of retirement a beneficiary would be seeing a benefit that is roughly 4.5 percent lower as a result of the Bowles-Simpson plan. The plan also phased in an increase in the age for receiving full benefits to 69, which is also a benefit cut for lower income retirees.

For lower income retirees Social Security is the overwhelming majority of their income. This means that the benefit cut advocated by Bowles and Simpson would imply the loss of a much larger share of their income than the end of the Bush tax cuts would for the wealthy. However, the Post has never described the ending of these tax cuts as a “modest” or “small” tax increase.

Now the current version of the Cat Food Commission, the Congressional Super Committee is about to use cutting Social Security as a publicity stunt to show how serious they are about cutting the deficit. The cuts are on the table because, as Jeff Madrick points out, the stupid Democrats think that their Republican counterparts on the committee will agree to raising taxes. In his article makes it very clear that the burden of these “deficit reducing proposals” will fall on the backs of the most vulnerable in our society, the elderly:

So let’s be clear. The Social Security Administration projects that benefits will rise by one percent of GDP from five percent to six percent over the next 20 years or so and then stabilize or even fall a bit due to the rising elderly population. One percent. That’s what all this is about.

snip

Let me also remind us that Social Security is not very generous. The average payment is $14,000 a year. It is getting less generous. It used to replace 55 percent of retirement income, but benefits were reduced in the 1980s. It now covers on average 41 percent of retirement income. In 2031, it will cover 32 percent of retirement income.

We have already reduced the program’s generosity. Yet, Social Security provides nearly all income for one quarter of the elderly and more than half the income for more than half of the elderly.

The Super Committee will say it simply wants to make the inflation calculation more accurate. It will reduce benefits. But government research suggests elderly costs rise faster in price than the traditional measures of inflation.

snip

What will drive future budget deficits is Medicare and Medicaid, not Social Security, and for the umpteenth time, the reason is that overall health costs are expected to rise quickly. This means we have to reform our uniquely inefficient healthcare system. Congress is, as usual, diverting us from the real issues. No wonder Americans like Occupy Wall Street.

Recent Comments